Autodesk (ADSK) shares took a hard hit after projecting a disappointing outlook even after beating earnings and sales expectations. Today, I take a closer look at what may have caused the >10% dip in share price.

Overview

- Autodesk, Inc. is a software company that makes products for the architecture, engineering, construction, manufacturing, media, education, and entertainment industries.

- The company’s customers design, fabricate, manufacture, and build anything by visualizing, simulating, and analyzing real-world performance early in the design process.

- Autodesk’s products are sold globally, both directly to customers and through a network of resellers and distributors.

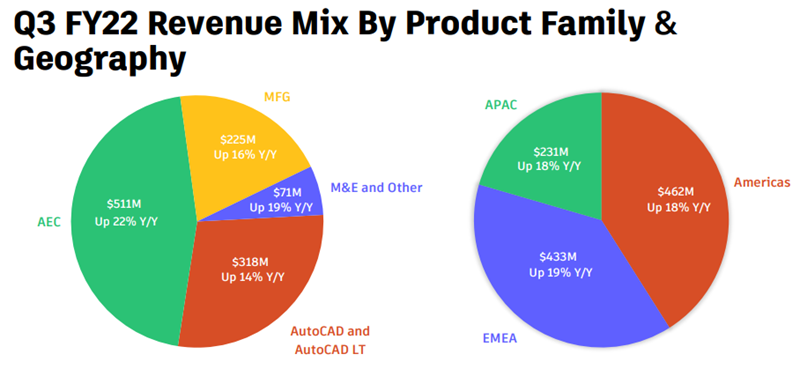

- The product offerings are sold through a subscription model and it’s broken into four main categories including:

- Architecture, Engineering, and Construction (AEC)

- AutoCAD and AutoCAD LT

- Manufacturing (MFG)

- Media and Entertainment (M&E)

- In 2017, Autodesk started a program to incentivize maintenance plan customers to move to subscription plan offerings, maintenance-to-subscription (M2S). In the most recent quarter, subscription revenue makes up over 95% of total revenue versus maintenance revenue making up ~1.5% of total revenue.

- Autodesk recently held its 2021 Investor Day in September.

Q3 Earnings Highlights

Financials

- Revenue | Increased 18% YoY to $1.13 billion, meeting analyst expectations.

- Recurring revenue represents 97% of total revenue.

- Total Billings | Increased 16% YoY to $1.17 billion.

- Net revenue retention rate | Stayed within the target range of 100% – 110%.

- Operating income

- GAAP: $193 million (17% margin, down one percentage point YoY).

- Non-GAAP: $365 million (32% margin, up 2 percentage points YoY).

- Cash flow from operating activities | $270 million, decrease of $91 million from last year’s Q3.

- Free cash flow | $257 million, decrease of $83 million from last year’s Q3.

Management Commentary

Andrew Anagnost, President + CEO

“Our customers continue to embrace and prioritize digital transformation to drive growth, efficiency, and sustainability, generating strong demand for Autodesk’s platform.”

- On why supply chain disruptions impact Autodesk: “While demand is robust, we believe supply chain disruption and resulting inflationary pressures, a global labor shortage, making it harder for our customers to staff new projects and the ebb and flow of COVID are contributing to the deceleration as well as documented country-specific disruption to AEC in China.”

- On sustainability as a tailwind: “Sustainability needs to be designed, made and, in many cases, retrofitted in construction and manufacturing. This cannot be achieved efficiently or effectively without end-to-end software like ours to drive the process.”

Debbie Clifford, CFO

“Demand was robust in Q3, driving strong new subscriptions growth and renewal rates. We expect it to remain so in Q4. However, supply chain disruption and resulting inflationary pressures, a global labor shortage, and the ebb and flow of COVID are impacting the pace of our recovery and outlook.”

- On the shift to direct revenue: “About 3/4 of new customers Autodesk are now generated through our digital channels, reflecting the strength of our simplified buying experiences. Our product subscription renewal rates reached record highs, and our net revenue retention rate was toward the high end of our 100% to 110% range.”

- On share repurchases: “We continue to repurchase shares to offset dilution from our equity plans. During the third quarter, we purchased 980,000 shares for $287 million at an average price of approximately $293 per share. Year-to-date, we’ve repurchased 1.66 million shares at an average price of approximately $287 per share for total spend of $476 million.”

- On future cash flow targets: “We continue to target $2.4 billion of free cash flow in fiscal ’23 in constant currency because we believe the current macro headwinds we’re seeing are transient.”

- On future targets: “We remain optimistic about our growth potential beyond fiscal ’23, continue to target double-digit revenue growth, non-GAAP operating margins in the 38% to 40% range and double-digit free cash flow growth on a compound annual basis.”

Guidance

“In light of this macroeconomic uncertainty, as we enter Q4, we’re taking a pragmatic approach and are assuming that the supply chain, labor, COVID, and country-specific challenges will persist. As a result, we’re reducing the midpoint of our billings and free cash flow guidance by approximately $150 million and $100 million, respectively, for full-year fiscal ’22. Given the nature of our subscription business model and the greater degree of near-term visibility, it provides to us and our expectation of continued strong spend discipline, the midpoint of our full-year revenue and margin guidance is broadly unchanged.”

Valuation

- Autodesk shares have been beaten down to ~$263 per share in pre-market trading.

- Accounting for the number of diluted shares outstanding provided by the company, ADSK is trading at a $58.5 billion market cap.

- After adding net debt, the enterprise value of the company is $59.3 billion.

- Using analyst estimates from Sentieo, ADSK is trading ~13x forward gross profit and ~31x forward adjusted EBITDA.

Authors Review

MH: Autodesk products cover a number of verticals in design and infrastructure. The company even has project management tools specifically for the industries it serves. Nearly half of the revenue pie comes from Architecture, Engineering, and Construction (AEC) which may benefit from the newly signed infrastructure bill. But it’s important to note that Autodesk’s business is not centralized in the United States. Management specifically called out potential headwinds in its China market and near-term headwinds from supply chain issues. At first, I questioned why supply chain issues would impact a software maker, but this software is mostly deployed for physical projects requiring workers and we are in the midst of a worker shortage.

Autodesk is optimistic about its growth potential beyond FY23, targeting double-digit revenue growth and non-GAAP operating margins in the high 30s with strong cash flows. However, the cautious tone and guidance from management in the most recent quarter spooked investors after-hours.

Autodesk’s valuation is in-line with other SaaS companies at the moment, so an investment here would require some differentiated bullish view on the future demand for architecture and EPC software. And since its guided growth of mid-teens isn’t particularly exciting, I think there are probably more-obvious investments out there.